When I look at the 2nd Screen industry trends today, I can’t help but think back to what we were focused on only 12 months ago as we prepared to come together at CES in Las Vegas. We spent a lot of time talking about Social TV, the consolidation of the industry, ACR, and whether or not consumers were actually using their 2nd Screen devices to engage with there video content—or just to play Angry Birds.

During the last year, we tracked the important figures that defined each quarter:

- · Q4 2012. 35 million tablets sold in the U.S. alone during the Christmas rush and significant social TV and 2nd Screen engagement growth in all scenarios.

- · Q1 2013. Clear evidence of “t-commerce” from 2nd Screens and the continued growth of active zeebox and Viggle subscribers—bell weathers for the industry on consumer engagement in 2nd Screen.

- · Q2 2013. Hyper growth in mobile video viewing, especially in ad supported—a key trend to observe for the potential of 2nd Screen monetization in converged experiences.

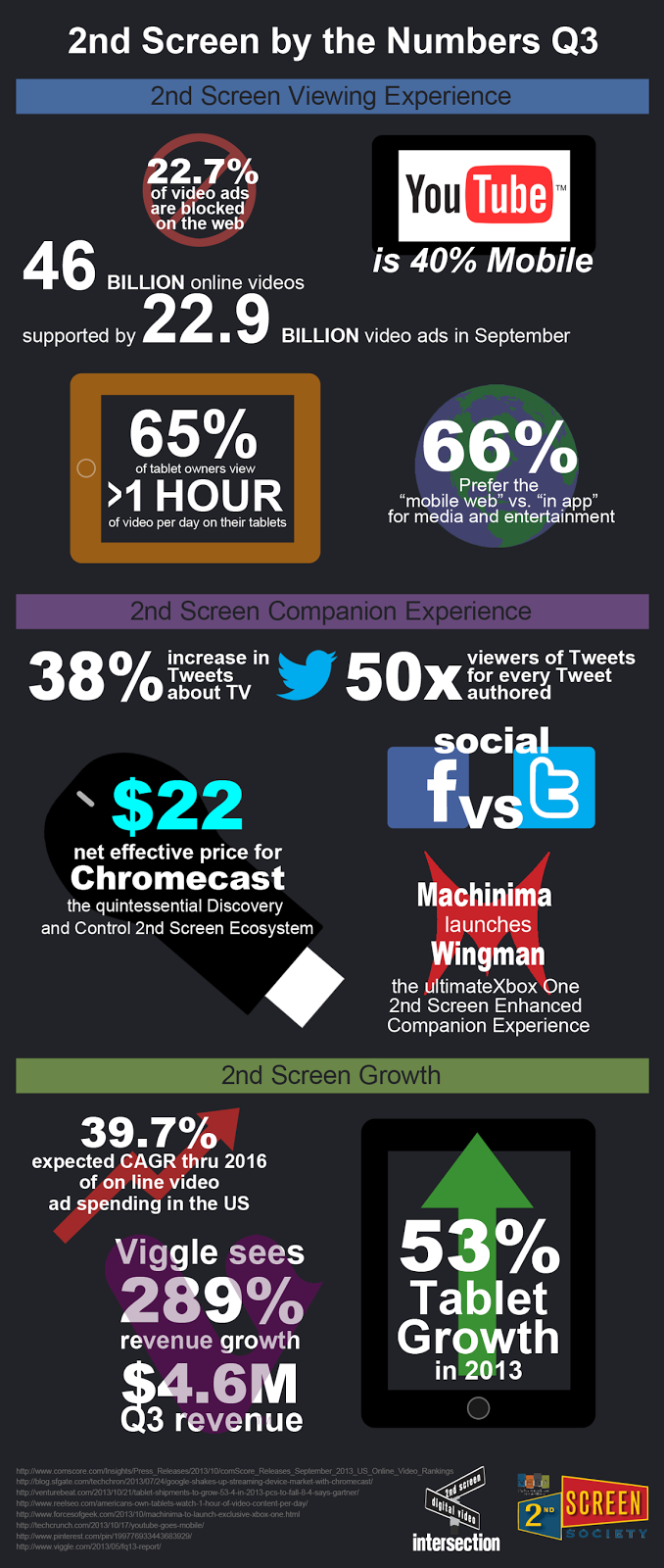

- · Q3 2013. Continued viewing growth on mobile, strong revenue growth from enhanced 2ndScreen engagement apps and the launch of Chromecast—an opportunity for any 2ndScreen app developer to give Discovery and 1st screen Control capabilities to their video viewing experience.

We started last year by identifying 10 potential trends to watch for in the industry, some of which quickly became self-evident and some of which did not materialize. Of course some unanticipated trends revealed themselves along the way. We think the most impactful trends for our industry right now are:

· An “ecosystem” not an app. Success in consumer engagement Microsoft’s Xbox Smartglass and Google’s Chromecast are the best current examples in this space. For Smartglass, there is one app which reveals all 2nd Screen companion experiences for video, music and games in their content ecosystem. For Chromecast, they have found a way to give app developers the ability through the DIAL protocol to leverage control of the 1st screen, combining Discovery and Control capabilities across the app ecosystem and freeing up the device for Enhanced Viewing and Social experiences. Expect Netflix and Apple to do something here quickly.

· An “ecosystem” not an app. Success in consumer engagement Microsoft’s Xbox Smartglass and Google’s Chromecast are the best current examples in this space. For Smartglass, there is one app which reveals all 2nd Screen companion experiences for video, music and games in their content ecosystem. For Chromecast, they have found a way to give app developers the ability through the DIAL protocol to leverage control of the 1st screen, combining Discovery and Control capabilities across the app ecosystem and freeing up the device for Enhanced Viewing and Social experiences. Expect Netflix and Apple to do something here quickly.· Convergence of companion and viewing experiences. This trend will continue to develop a millennials choose mobile devices over the living room and because it is by far the leading monetization opportunity – inline video advertising. As the ability to click thru ads continues to grow, this will become a more and more valuable opportunity for all members of the ecosystem.

· Ad supported video on mobile devices. Today, while the total spend in this space is somewhere between 1-3% of total TV advertising spend (roughly $6 billion in 2013), it continues to grow at a breathtaking pace (25%+ CAGR) and TV networks are beginning to find higher CPM pricing for tablets and smartphones than they are for the living room TV (digital or analog). This is attributable both the highly targetable nature of a 2nd Screen (often not shared with others) and the easy interactive capabilities (the ability to click thru to more information during a video ad).

· Monetization. You don’t have to look very far to find revenue success in this space as 3rd party Enhanced Viewing experience app Viggle is a publicly traded company, reporting $4.6 million in revenue for most recently publish quarter—which was a growth of 289% on the prior 12 months. Assuming they continue to grow even at a modest pace, they will be able to deliver more than $20 million in revenue in 2014.

· The rise of HTML 5. In the past 12 months, a significant trend has developed in mobile where 66% of consumers are now choosing to engagement in their entertainment content through their mobile browser rather than through an app. This means developing responsive HTML 5 apps is more important than ever for both in app and “mobile web” 2nd Screen experiences for the consumer.

· The rise ad blockers. Once a desktop only problem, there are companies who are focused on building feature sets that allow consumers to circumvent the most successful monetization approach in this space—blocking display and video ads. Development of this trend and approaches to thwart its impact on 2nd Screen companion and viewing experiences is paramount to the success of the ecosystem.

However, despite the continuous positive points of data revealing themselves along the way, the industry finds itself in a precarious place—somewhere between the “Peak of Inflated Expectations” and the “Trough of Disillusionment” (to quote Gartner’s Hype Cycle terminology). Analysts and trade press are now keying in on failed experiences nearly as often as successes, all archived in our twice weekly 2nd Screen 2Day new letter. Combine that with the natural consolidation of the startups in the industry (which includes failed ventures), and it is easy to find yourself being more disillusioned than hyped.

Our responsibility as an industry association is to help our members focus on the key elements of success that can drive their business forward. So as we prepare for the 2014 CES 2nd Screen Summit, we will drive our efforts towards the three primary business drivers which should represent every member of our ecosystem:

- 1. Increased consumer engagement in the content. The majority of the investment in 2nd Screen companion and viewing experiences is coming from the content creators and distributors (primarily the TV networks). Creating a lift in engagement (i.e. viewing time) translates to increased revenue regardless of their monetization model.

- 2. Increased consumer engagement with the advertising brands. The vast majority of the content ecosystem focused on 2nd Screen monetized their content through advertising in some form. As major brands place bets in this space, they are focused on metrics like “Cost per Touch” instead of impressions delivered (CPM). The brands crave interactivity and engagement, working to determine which consumers are interested enough to move forward in their purchase cycle.

- 3. Monetization itself. While major TV networks and brand advertisers can get comfortable with metrics that have a strong correlation to monetization, many of the 1st and 3rd party engagement developers depend on revenue coming in the door to support their investments—“where the rubber meets the road” so to speak, as actual payments for advertising, t-commerce and engagement come together in the 2ndScreen companion and viewing experiences.

To support the 2nd Screen Society members in this journey up the “Slope of enlightenment”, we are going to focus both our research and our conference engagement topics along these three major business drivers. First, we are going to make our research more readily available to members, developing case studies in the industry helping to reveal tangible evidence of success in these three areas. Second, as we identify, track and engage in industry trends, we are going to do so in a manner that helps reveal the impact on these three important business models.

I am looking forward to watching the industry grow and develop towards the great potential we all identified many, many months ago.

See you in Vegas!

Regards,

Chuck

@ChuckParkerTech